Record volume, falling prices: a snapshot of the avocado summer in Europe

From June to August, the European avocado market enters a predictable but challenging cycle. This is the period when the volume of fruit from the Southern Hemisphere reaches its peak, and prices tend to fall under supply pressure. Data from Avobook, obtained from its Data and Analytics department, confirms that between 2023 and 2025 this pattern has remained clear: when shipment volumes to Europe increase, weighted average prices in Rotterdam decline.

Avobook's analysis is based on weeks 18 to 35, spanning May to August, considering the weighted average price per kilogram in US dollars for size 18 in Rotterdam and the number of weekly containers. Comparative graphs illustrate how, in each season, the price curve forms a "V" shape, coinciding with the increase in shipments from South America, especially from Peru.

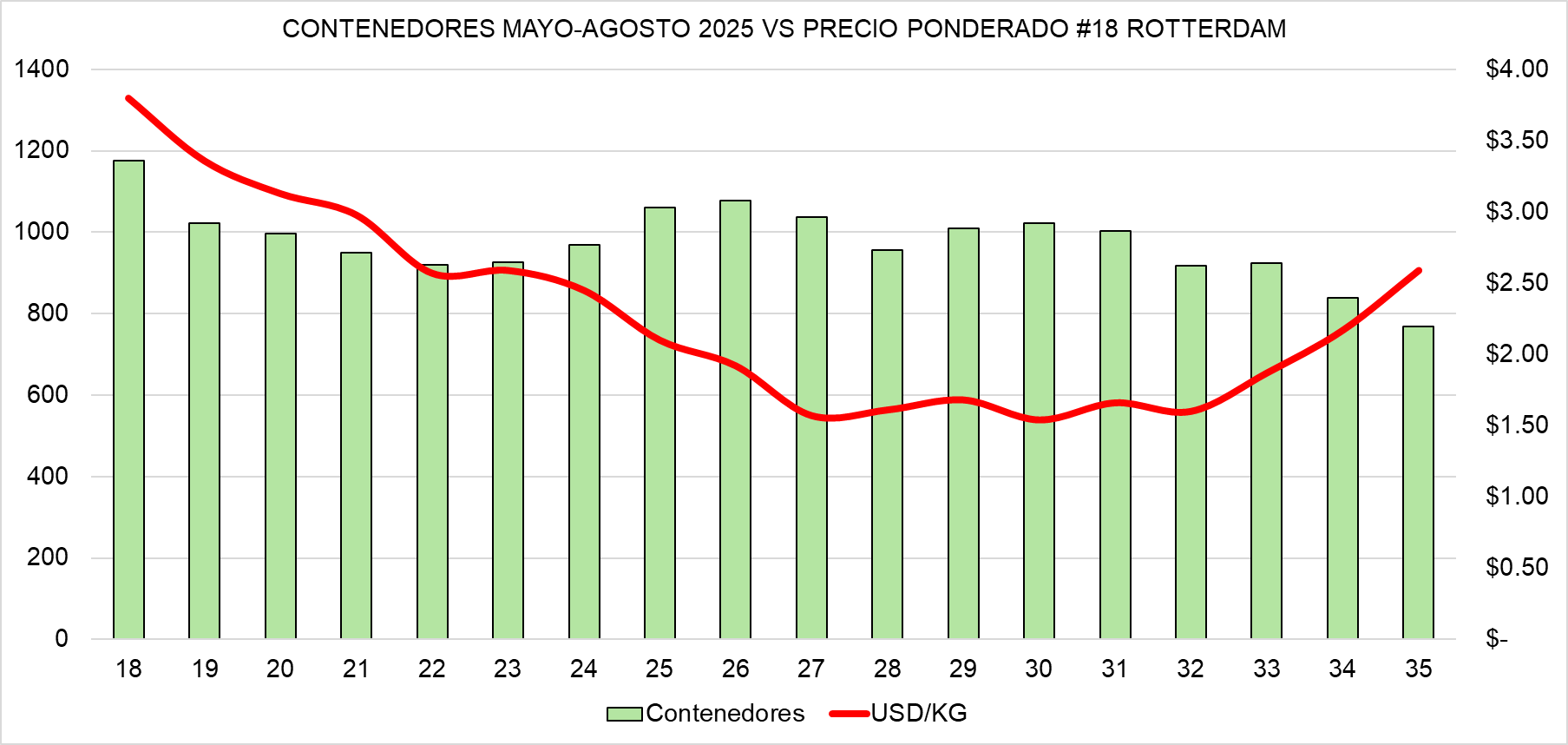

2025: the sharpest decline

In 2025, the price began to decline from week 18, reflecting a market that was already highly supplied. The drop intensified during the middle of the season and reached its lowest point at the beginning of the second half, coinciding with the period of highest concentration of arrivals at the port of Rotterdam.

Starting in weeks 33 and 34, Avobook's data shows a price rebound. This change occurred at the same time that export volumes from Peru began to decline. The relationship is direct: less available supply leads to a greater price recovery. "The lowest point was recorded at the beginning of the second half of the year, with a few weeks of stability until prices rebounded, just as shipping volumes from Peru began to decrease," explains Avobook's analysis team.

The pattern is that of a classic "V" of saturation, in which the excess of containers in the European market pushes values down until the logistics flow normalizes.

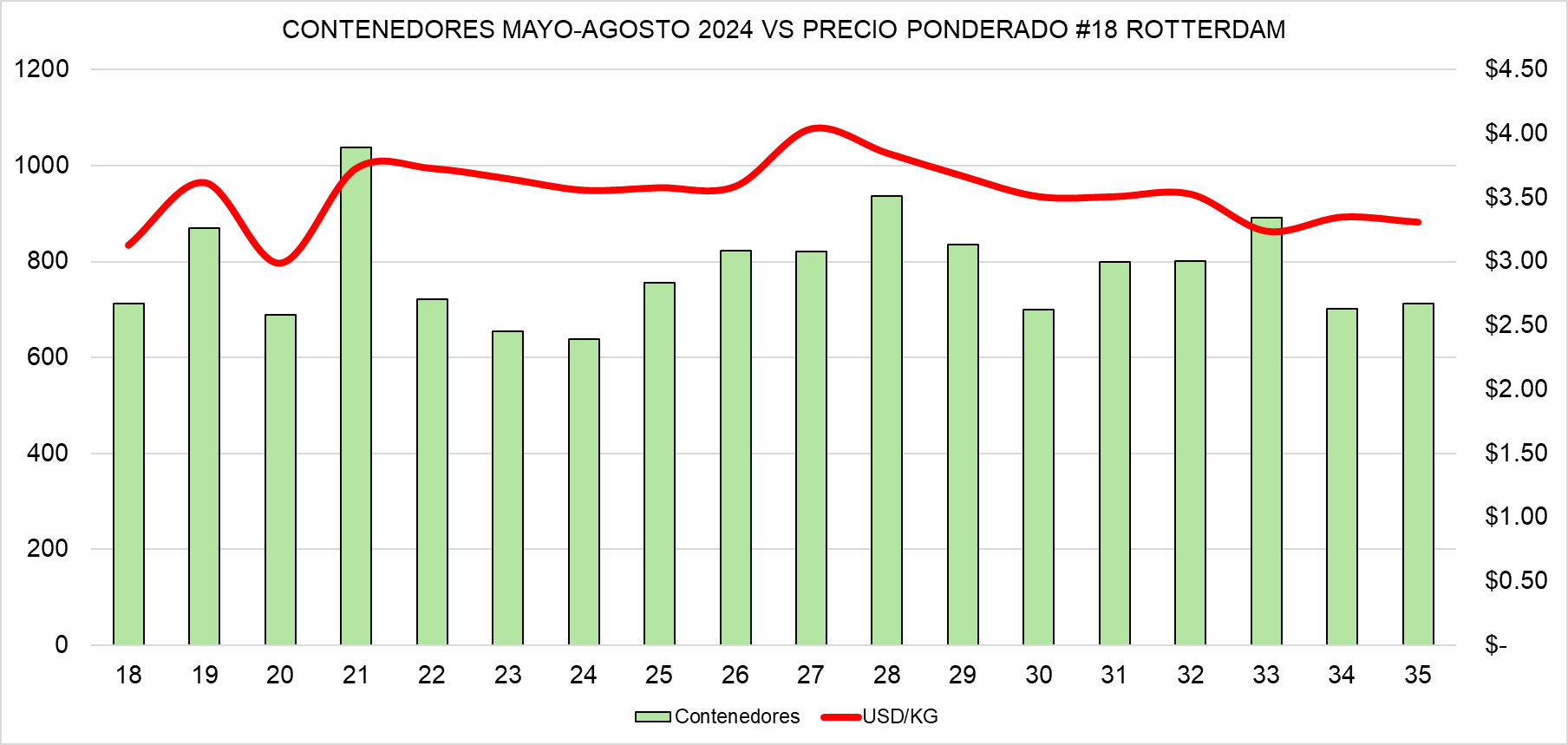

2024: Even prices and a more balanced market

The year 2024 showed a different trend. Prices remained relatively stable and with less variation than in 2023 or 2025. According to Avobook's records, the price curve remained "even," without abrupt drops, despite fluctuations in weekly volumes.

This stability reflects a scenario of strong demand in Europe, where ripening programs and consumption promotions helped absorb the fruit without a significant drop in average prices. According to the CBI – the Netherlands Ministry of Foreign Affairs, summer prices are typically lower due to abundant supply, especially from Peru, but factors such as fruit quality, trade coordination, and size management can mitigate the impact. “Summer prices are generally lower due to the increased supply, particularly from Peru, and the overlap with South Africa and Kenya,” the European agency's report states.

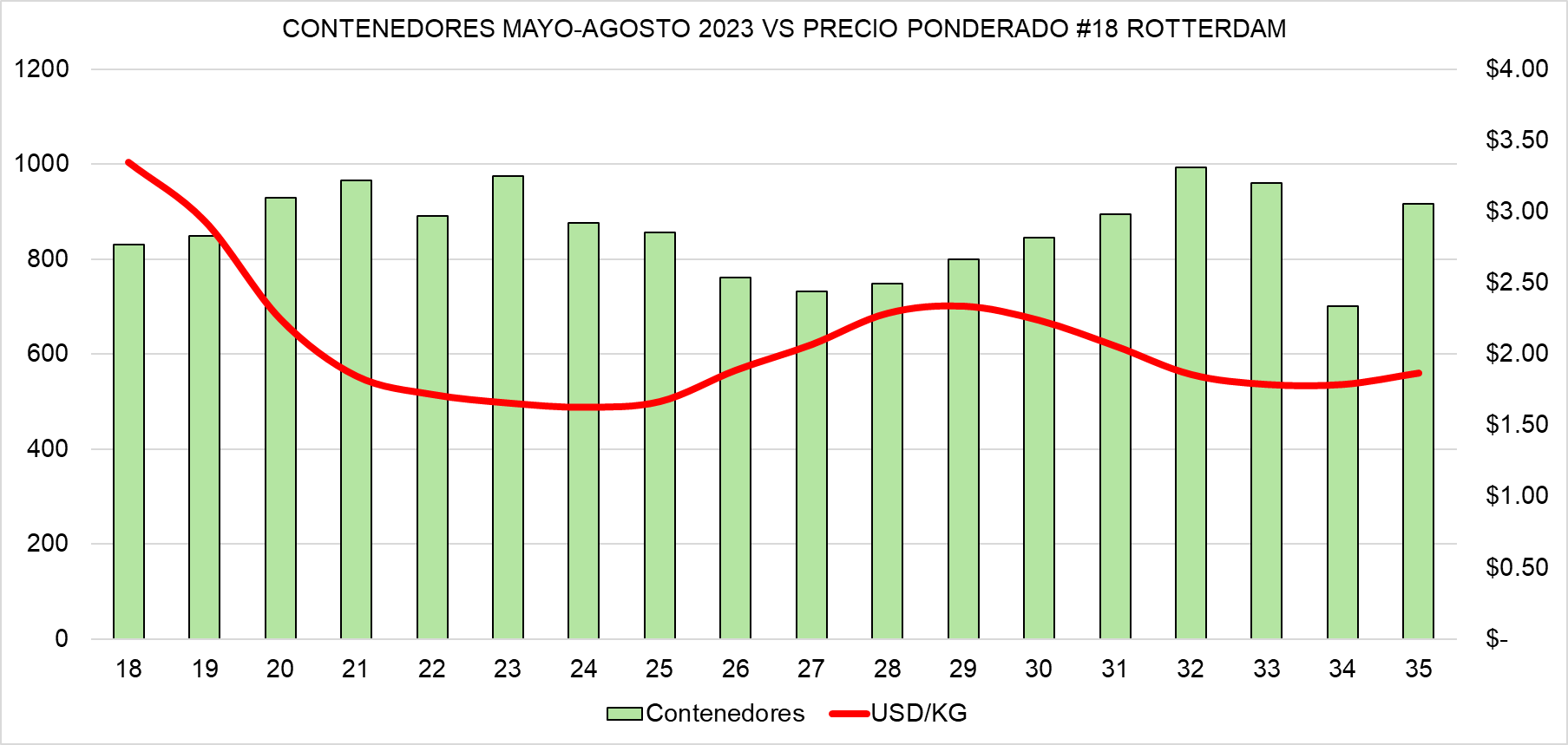

2023: Early declines and partial recovery

In 2023, the price curve exhibited mixed dynamics. Prices began to fall in May, bottomed out in early June, and experienced a slight recovery around weeks 28 and 30, even though weekly volumes remained high. This temporary recovery coincided with an adjustment in size composition and increased marketing efforts by European supermarkets, which promoted product turnover through special pricing campaigns. Towards the end of August, however, the market again showed signs of weakness.

Avobook's analysis shows that the impact of volume on price was high in 2025, moderate in 2023, and low in 2024. In all cases, the relationship is negative: when container shipments exceed the historical average, prices tend to fall.

This phenomenon is also supported by official data. According to Eurostat/Comext, in 2023 the European Union imported 756,800 tons of avocados, of which 312,800 tons came from Peru, its main supplier during the summer months. Records from the Réseau des Nouvelles des Marchés (RNM) of FranceAgriMer show a downward seasonality in Hass wholesale prices at the Rungis market during the same period, with marked declines between June and August. The Bundesanstalt für Landwirtschaft und Ernährung (BLE) in Germany reports a similar trend in its weekly reports on fruit and vegetable prices.

Can consumption compensate for excess supply?

Although European avocado consumption maintains an upward trend —driven by the consolidation of the product in large distribution channels—, CBI reports warn that demand is not growing at the same rate as exports and that episodes of oversupply will continue to cause price fluctuations.

“Prices are not stable and oversupply tends to recur more frequently,” the organization notes. The curve observed in 2025 reflects precisely that warning: consumption is growing, but not enough to absorb production peaks concentrated in just a few weeks.

Looking ahead to the next seasons, the main challenge will be planning shipments to avoid seasonal saturation. Avobook analysts suggest that coordination between producers and exporters will be essential to balance the weekly flow of shipments to Europe and reduce the impact on prices.

Experts recommend spacing shipments between weeks 24 and 31, adjusting sizes to consumer preferences, and reinforcing supermarket promotions during peak periods. Official statistics—such as Eurostat/Comext databases, FranceAgriMer reports, and BLE publications—can also serve as monitoring tools to anticipate saturation weeks and make tactical decisions in real time.

In short, Avobook's analysis and official sources agree on one conclusion: the European summer remains a test of the balance between volume and price. While consumption maintains a positive trajectory, the market's capacity to absorb large volumes in a short period remains limited. And although 2024 showed that stability is possible, 2025 made it clear once again that abundance comes at a cost: an inevitable decline in the value of avocados in Europe.