A market with excess volume and prices that aren't picking up: an X-ray of the avocado market in the United States

The US market is experiencing a period of intense pressure from oversupply, led by Mexico, while consumption slows. According to experts and data from Avobook, the recovery could take until December.

The avocado market in the United States is facing a complex situation. The combination of an exceptionally high supply and weaker-than-usual demand has led to a significant drop in prices, affecting the entire value chain.

The oversupply comes primarily from Mexico, which is exporting at near-record levels. This is compounded by regular shipments from Colombia and Chile, as well as some remaining stock from California. The result, according to Gary Clevenger of Freska Produce International, is a market overwhelmed by volume.

“The U.S. avocado market is experiencing significant pressure due to high supply, particularly from Mexico, which is shipping fruit at a near-record pace,” Clevenger explains. “Add to that the steady flows from Colombia, Chile, and some final shipments from California, creating an oversupplied market that far exceeds consumer demand.”

This fruit surplus has caused congestion at storage and distribution centers, where product movement has slowed. “Buyers are being very selective, forcing packers and importers to lower prices simply to keep things flowing,” the executive explains. Normally, this volume could be absorbed through promotions and retail offers, but the current situation isn't helping: consumption is cooling, and there's a risk that a potential U.S. government shutdown could disrupt SNAP benefits, a crucial program for low-income households.

The result is a market under pressure at all levels. With current prices, producers' profits have been reduced to a minimum. "Many producers, especially small ones in Mexico, are barely covering harvesting and packing costs," Clevenger acknowledges. "If these conditions continue through November, some might stop harvesting to avoid a further price collapse, although that also carries risks, since the fruit continues to ripen on the tree."

According to Clevenger, markets driven by oversupply tend to correct themselves within four to six weeks as volume decreases and promotions strengthen. However, the pace of recovery will depend on demand. “If the government shutdown continues and food assistance funds stop circulating, consumption will remain weak, prolonging the low-price environment. The market could remain under pressure well into December before showing any real improvement,” he warns.

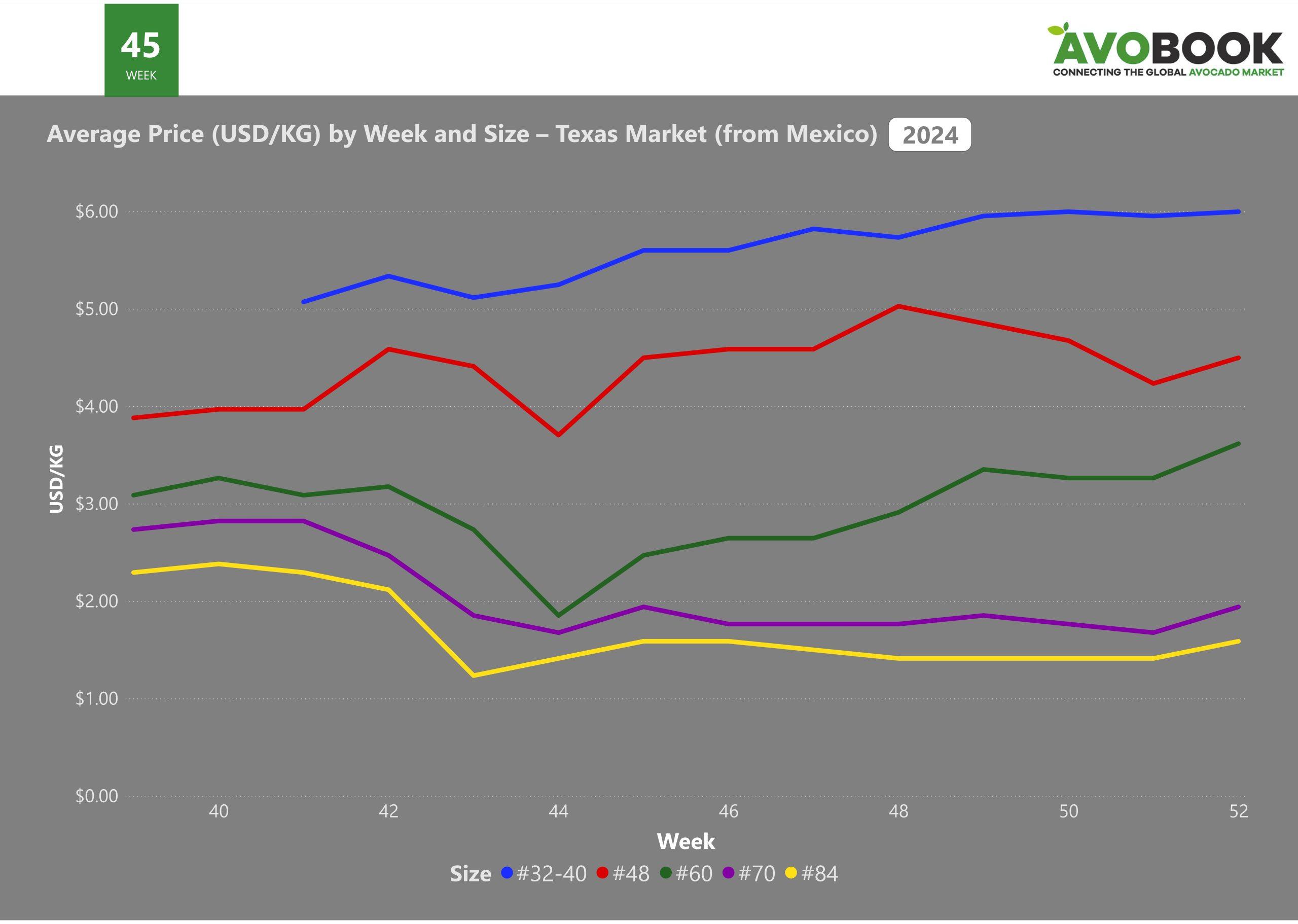

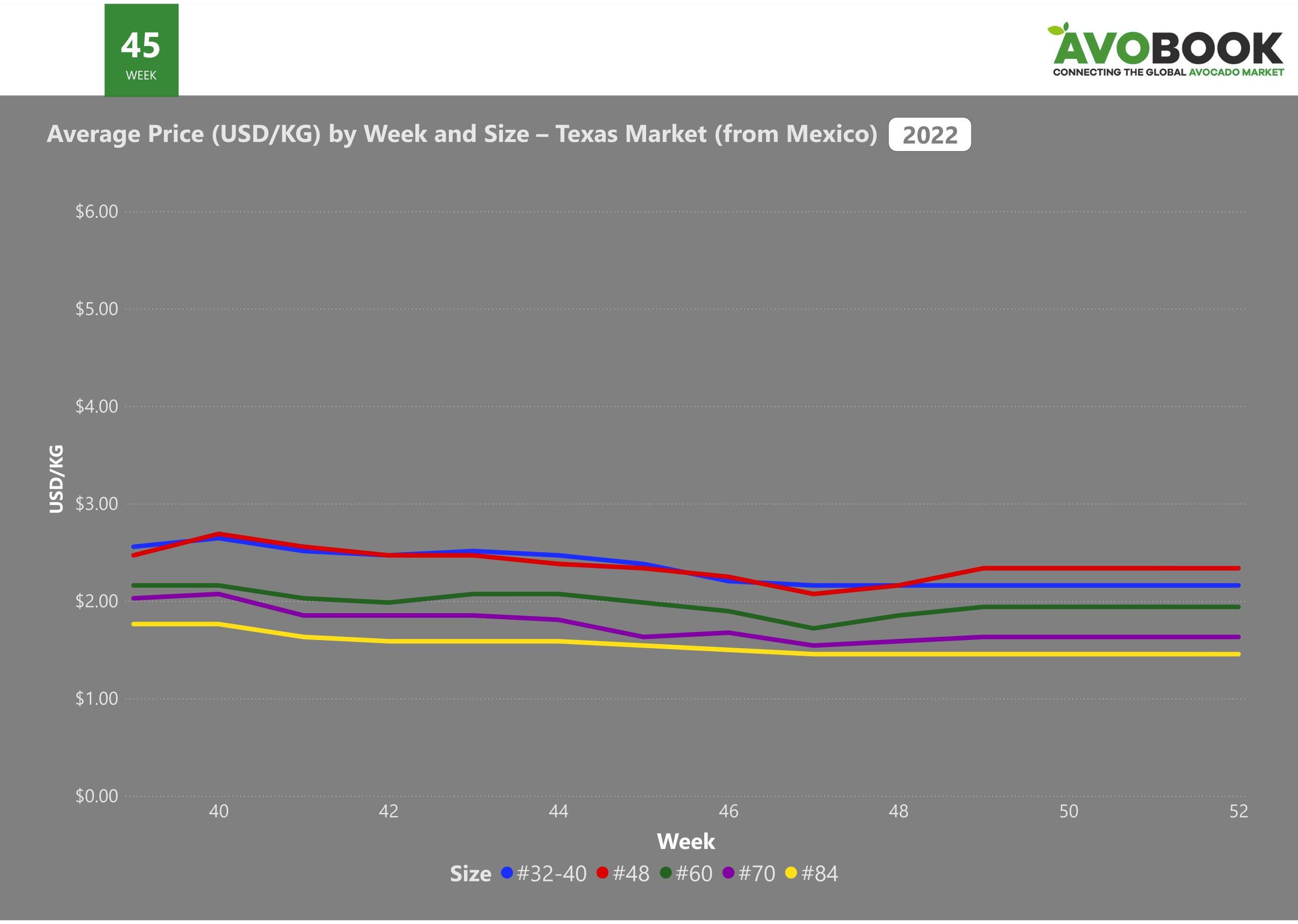

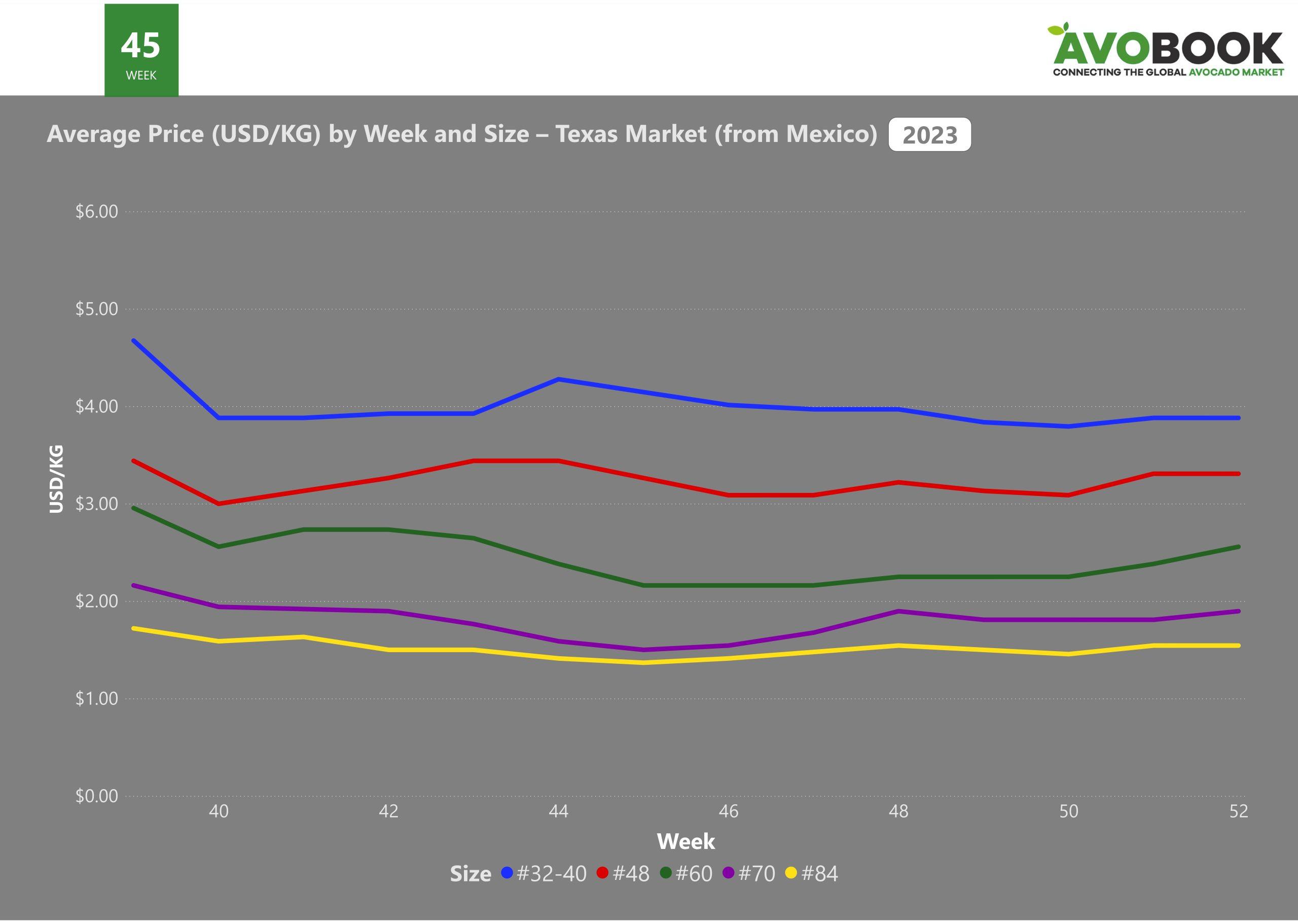

One of the most visible aspects of this situation is the loss of the traditional size differential. Larger sizes—32s to 40s—have been the most difficult to sell, affected by the decline in demand in the foodservice channel and high-end supermarkets. In contrast, smaller sizes (60s to 84s) are maintaining somewhat better sales thanks to bag programs and consumers seeking more economical alternatives. However, even in these sizes, prices are well below normal levels. “The price differential between sizes has narrowed dramatically. The market is soft across all sizes, and the traditional size premium has virtually disappeared,” Clevenger notes.

Data that confirms the trend

Avobook Data helps to put this behavior into historical perspective. In the fourth quarter of 2024, the market showed a strong divergence between sizes: large sizes saw price increases, while small sizes maintained a downward trend, with weekly differences exceeding $4.5 USD/kg between the extremes.

In contrast, in 2022, the gap was minimal: the prices of the different sizes remained very close, not exceeding a difference of 1 USD/kg in any week of the quarter.

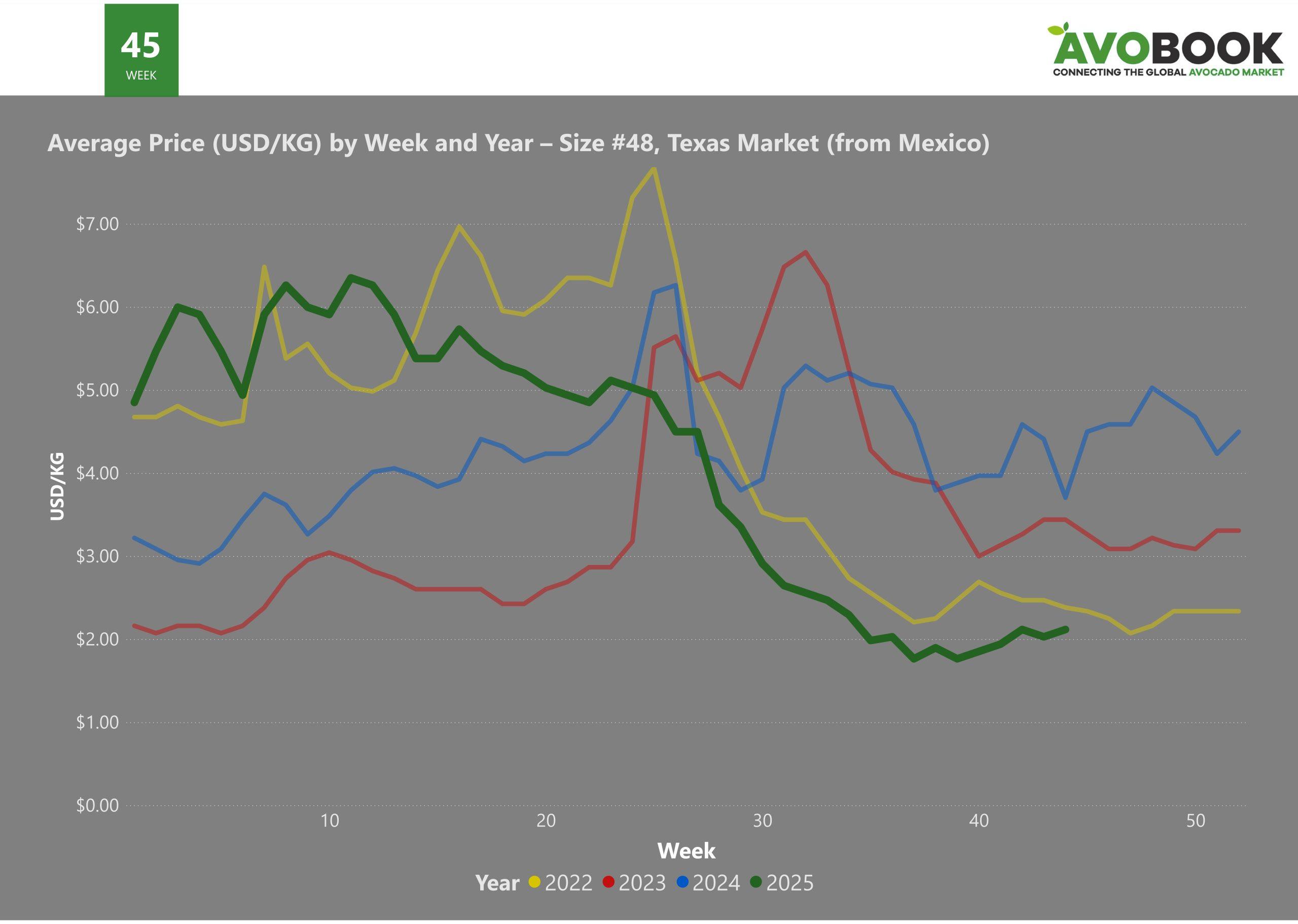

The year-over-year analysis of the .48 caliber—a benchmark for the U.S. market—confirms this trend. This year, its prices have followed a pattern very similar to that of 2022, with considerably lower values than in 2023 and 2024. In several recent weeks, the price of the .48 caliber didn't even reach half the levels recorded in the previous two years, clearly reflecting the magnitude of the decline.

At the operational level, the situation is exacerbated by other factors. The California season is practically over, eliminating the domestic supply that usually acts as a market buffer. At the same time, weather conditions in Mexico have been favorable, allowing for a harvest at full capacity. Furthermore, retail prices at the point of sale have not fallen at the same rate as FOB prices, preventing demand from reacting more quickly.

Despite this outlook, the forecast isn't entirely negative. With the final quarter progressing and the start of year-end promotional programs, supply and demand are expected to find a better balance. "The market will likely remain weak during November, but could begin to improve toward December or early January, as the programs stabilize and promotional volume increases," Clevenger projects.

Meanwhile, the US avocado market is experiencing a year-end marked by abundance, caution, and uncertainty. The speed of the recovery will ultimately depend on a delicate balance between the pace of the harvest, consumer purchasing power, and the system's capacity to absorb the fruit without becoming saturated again.