Chile exits the Chinese market while Peru accelerates its shipments.

Peru accelerates shipments to China while Chile reduces its presence

Chile's exit from the market and the increase in shipments from Peru anticipate greater supply in China, with possible downward pressure on prices in March.

The Chinese avocado market is beginning to show a clear shift in its supply origin. While Chile is gradually reducing its shipments, Peru is starting to increase its presence, creating a scenario that could alter price behavior in the coming weeks.

According to Avobook's Data team, the change is already visible in the recent volumes arriving in the Asian market. Chile has begun to drop out of the supply chain: shipments fell from 27 containers in week 8 to 16 in week 9 and just 11 in week 10.

Meanwhile, Peru is experiencing a growing pace of shipments. The number of containers from Peru increased from 15 in week 5 to 35 in week 7, then to 48 in week 9 and 56 in week 10.

The trend suggests that the process is just beginning. In 2025, Peru continued to accelerate its shipments during this same period, exceeding 80 containers in week 13 and reaching more than 100 containers by week 16.

This gradual increase will be one of the key factors in understanding the evolution of the Chinese market in the short term. As Peruvian shipments approach the 80-100 container range per week, the available volume could begin to exert downward pressure on prices.

The trends observed in February are beginning to offer clues about how the market might behave in the coming weeks. According to an analysis by André Vargas, Global Procurement Manager at South American Express Co. and Commercial Director of Fruwer Produce LLC, February left a seemingly stable price scenario, but with signs of weakening real demand.

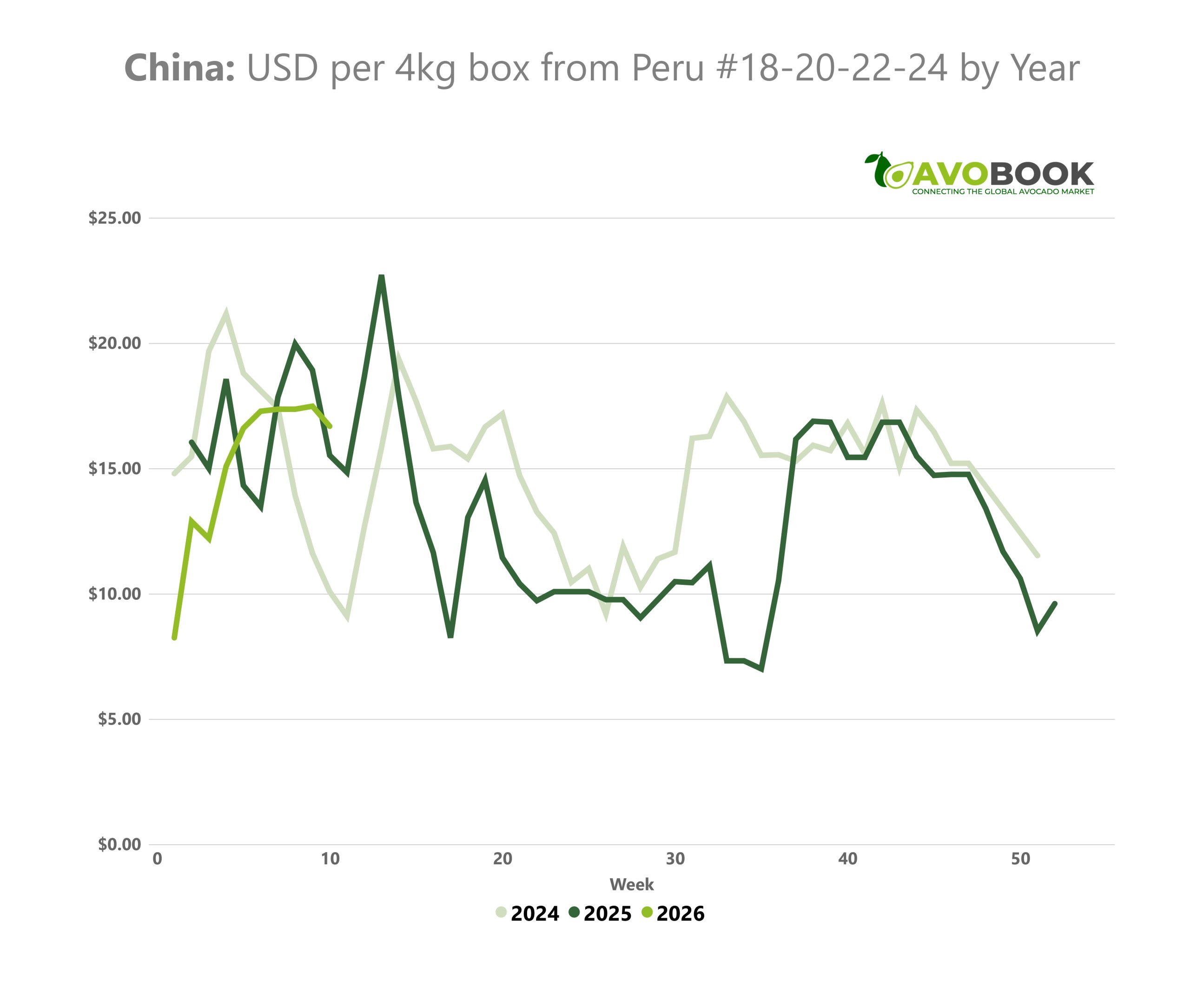

Following the Chinese New Year, the market experienced a gradual reopening. During weeks 5 and 6, prices remained relatively stable, hovering around RMB 240–250 for 10 kg boxes and between RMB 110 and 130 for 4 kg formats. However, beneath this stability, supply pressure began to build.

During those weeks, shipments from Peru to China reached 47 containers in week 5 and 57 in week 6. Although these volumes did not immediately affect prices at the destination, they did begin to build a scenario of greater future availability.

Week 7 was atypical due to the closure for the Chinese New Year holidays, with little commercial activity and prices that were not representative due to the low trading volume. In this context, the market showed an apparent firmness that, according to Vargas, did not necessarily reflect strong demand.

The market limit after the holidays

Week 8 marked the first real test after the holiday period. Upon reopening, an attempt was made to raise prices to RMB 150 for the 4kg format, but the market failed to sustain that level, closing mostly around RMB 130.

At the same time, the volume of shipments from Peru increased significantly. In that week alone, 81 containers left for China, driven in part by the departure of the vessel OOCL CHENNAI with 73 containers.

For Vargas, this increase in shipments is key to understanding the emerging scenario. Given that shipments from Peru take between three and four weeks to reach the Chinese market, the logistical decisions made in February directly impact the availability the market will face in March.

Week 9 already showed signs of correction. Prices displayed a wide range—between RMB 210 and 270 for 10 kg boxes and between RMB 90 and 140 for 4 kg formats—reflecting a less orderly market with more pronounced differences based on quality and inventory turnover.

The adjustment was primarily due to slower sales. According to Vargas, in the Chinese market the determining factor is not the opening price, but the product's turnover rate. When sales slow, price corrections can occur quickly.

In this context, the relatively high price observed immediately after the Chinese New Year was partly due to temporary factors: low available stock, operational closures, and some speculation in a market with little activity.

March: the key moment

The main focus now shifts to the arrival schedule that will take shape during March. Between weeks 5, 6, and 8, shipments departed from Peru totaling 185 containers, which should begin arriving in the Chinese market approximately three to four weeks later.

If these volumes arrive simultaneously, the market could face a significant increase in supply within a short period. In that scenario, buyers tend to adopt more defensive positions, which usually translates into rapid price adjustments and deeper discounts to clear inventory.

The evolution of this dynamic will depend on several factors, including the market's absorption capacity, the quality of the available fruit, and the rate at which the Peruvian supply continues to grow.

For now, the data shows that the shift in prominence between Chile and Peru is already underway in China, at a time when the market is beginning to prepare for an increase in volume that could set the tone for the season in the coming weeks.