The United States is on track for a historic import shutdown in 2025, with record volume and significant changes by origin.

The 2025 figures confirm a shift in the supply dynamics of the US market, where total volume reaches a new all-time high and the focus of growth is moving towards South America. While Mexico maintains its leading position without significant changes and California retains a stable role, the strong growth of Peru and the record-breaking performance of Colombia are redefining the composition of supply in the United States.

The 2025 figures confirm a shift in the supply dynamics of the US market, where total volume reaches a new all-time high and the focus of growth is moving towards South America. While Mexico maintains its leading position without significant changes and California retains a stable role, the strong growth of Peru and the record-breaking performance of Colombia are redefining the composition of supply in the United States.

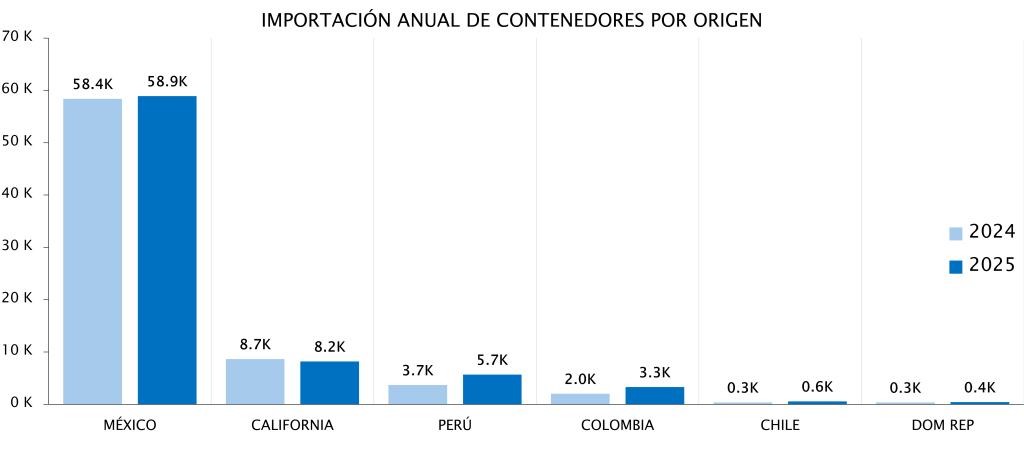

The US market is on track to close 2025 with the highest volume of imported fruit in its recent history. According to analysis by Avobook's Data & Analytics team, by the end of week 49, the cumulative total was already practically in line with the entire volume recorded in 2024, when 73,270 container equivalents were reached. With week 50 included and projections for weeks 51 and 52, the year not only surpasses that figure but also sets a new annual import record.

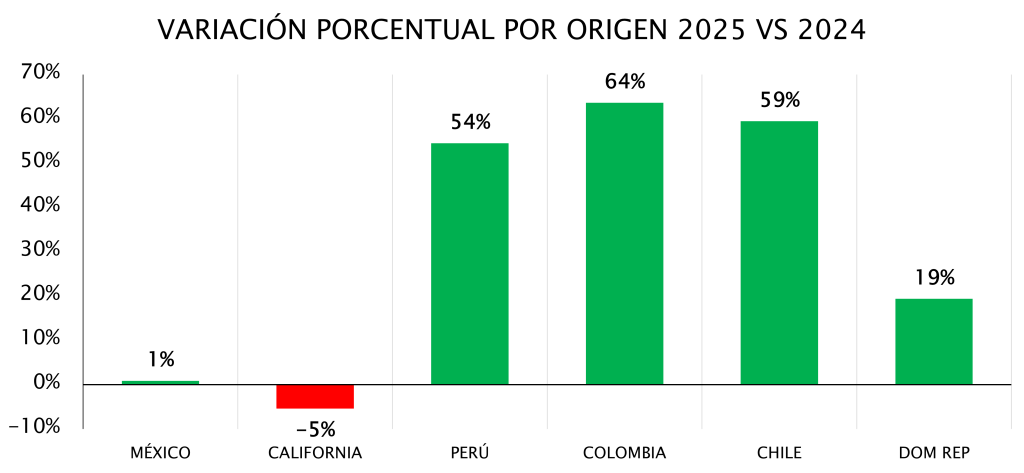

A comparative analysis between 2025 and 2024 shows that growth has not been uniform across different origins. Mexico maintains its position as the dominant supplier to the US market, although its year-over-year growth is marginal. Adding the year-end projections, the increase is around 1%, a limited variation that is more attributable to seasonality than to a lack of supply.

The explanation lies in the production calendar: while Mexico faces a large harvest, it only really took off between August and September. During the first part of the year, shipments were more limited and occurred within a context of higher prices, which restricted cumulative annual growth.

California, for its part, shows a performance that the Avobook team describes as relatively normal. With around 8,164 containers in 2025, the volume is slightly lower than the previous year, but remains clearly above what was observed in 2023. This performance allows it to consolidate its position as the second most important origin in the US market, with a share of approximately 10.6%, confirming its structural role within the local supply chain.

One of the most notable movements of the year comes from Peru. Fueled by a particularly abundant harvest, the country saw a significant increase in its shipments to the United States, becoming one of the main drivers of overall market growth in 2025. This expansion not only strengthens its presence in terms of volume but also demonstrates a greater ability to place its products in a highly competitive market.

Colombia also reached a milestone in 2025. By week 50, shipments had already reached 3,277 containers, setting a new record for this origin in the United States. Colombian growth stands out for both its pace and consistency, reflecting a sustained expansion strategy and greater integration within the trade flow to North America.

In contrast, other origins such as Chile and the Dominican Republic maintain a marginal share. Their volumes are so small that they barely impact the overall market analysis, relegating them to a secondary role in the annual balance.

Taken together, the data analyzed by Avobook confirm that 2025 will not only be remembered as a record year for total U.S. import volume, but also as a period of adjustments in the composition of origins. While Mexico maintains its leading position, real market growth has been driven by the strong performance of Peru and Colombia, in a context where seasonality, harvest size, and price dynamics explain much of the difference observed between 2024 and 2025.