European market

Small calibers are losing ground in Europe

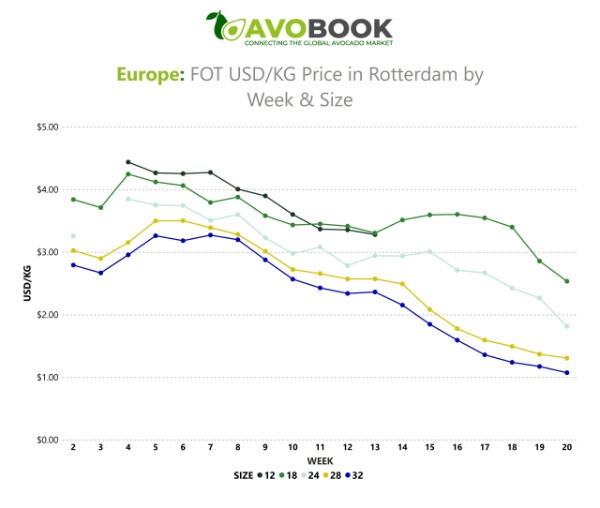

The surge in shipments hit the 28 and 32 calibers the hardest, while the larger sizes withstood the pressure better.

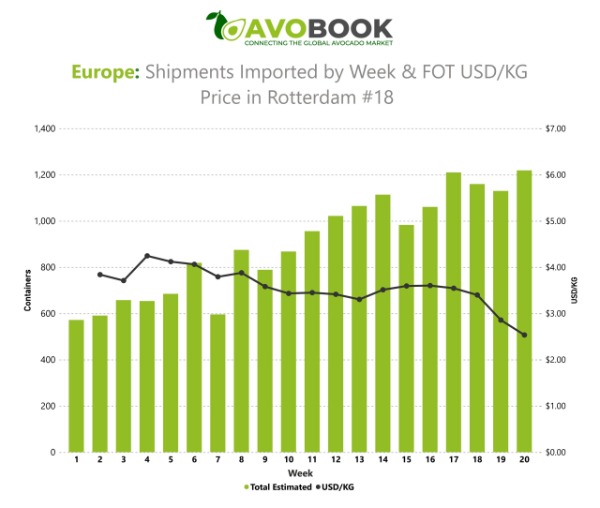

Weeks 17 and 18 marked another peak in the European avocado market, with over 1,200 shipments recorded and a similar dynamic to that observed last year. However, the impact on prices was not uniform. According to Avobook's data team, sizes 32 and 28 were the most affected, with prices beginning to decline more sharply from week 14 onward, coinciding with the sustained increase in arrivals to Europe.

Size 32 fell from levels close to USD 2.4/kg in week 14 to around USD 1.1/kg in week 20, while size 28 dropped from approximately USD 2.6/kg to USD 1.3/kg during the same period. In contrast, the larger sizes showed greater resilience: size 12 remained above USD 3.4/kg until week 18 and only showed a more marked decline towards weeks 19 and 20, while size 18 maintained higher values than the smaller sizes throughout the season.

The pressure increases with the peak of shipments

Avobook's analysis shows a clear correlation between the increase in weekly shipments and the drop in prices, especially for small and medium sizes. From week 11, arrivals grew from around 950 containers to over 1,200 in weeks 17 and 20. During that same period, prices began to weaken steadily.

The correlation was strongest in sizes 28 and 32, where the decline accelerated as the market received larger volumes. In contrast, larger sizes showed less sensitivity to the increase in supply, suggesting more stable demand and more limited availability. Furthermore, the market managed to maintain overall average prices between USD 3.3 and USD 3.6/kg until week 18, but a more abrupt correction appeared in weeks 19 and 20, coinciding with the peak supply.

During weeks 17 and 18, the difference between sizes was particularly evident. Sizes 28 and 32 traded under strong commercial pressure, with prices close to USD 1.6/kg and USD 1.3/kg, respectively. Meanwhile, size 12 remained around USD 3.5/kg and size 18 around USD 2.7/kg, reflecting that European retailers continued to show a preference for larger fruit even during weeks of high supply.

Peru and South Africa account for a large part of the supply

Peru appears to be the main source behind the pressure observed in Europe. Its shipments grew strongly from week 12, increasing from 247 containers to more than 660 between weeks 17 and 19, reaching 830 containers in week 20. This consolidated its position as the dominant supplier during the peak season.

South Africa also exerted significant pressure, growing from 39 containers in week 12 to a peak of 301 in week 17, maintaining a substantial presence during the weeks of highest supply. Brazil and Kenya also increased their volumes, albeit to a lesser extent, while Spain and Israel began to reduce their shipments. According to Avobook, California did not appear to have a significant share of these European import figures.

For now, the pressure seems to be due more to a temporary oversupply of fruit than to a structural change in European retail demand. The main indicator is that large sizes are still maintaining relatively strong prices, while the decline is concentrated in medium and small sizes, precisely those most abundant during the peak export season for Peru and South Africa.

Over the next few weeks, the gradual exit of some market players could help to stabilize supply. Peru is expected to remain the dominant supplier, along with some other origins, while South Africa is projected to continue sending consistent volumes. In this scenario, the performance of smaller-sized fruit will be key to gauging whether the current pressure is beginning to stabilize or if the European market will need more weeks to absorb the excess fruit.