Comparative analysis

Colombia stabilizes its avocado campaign and focuses shipments on Europe

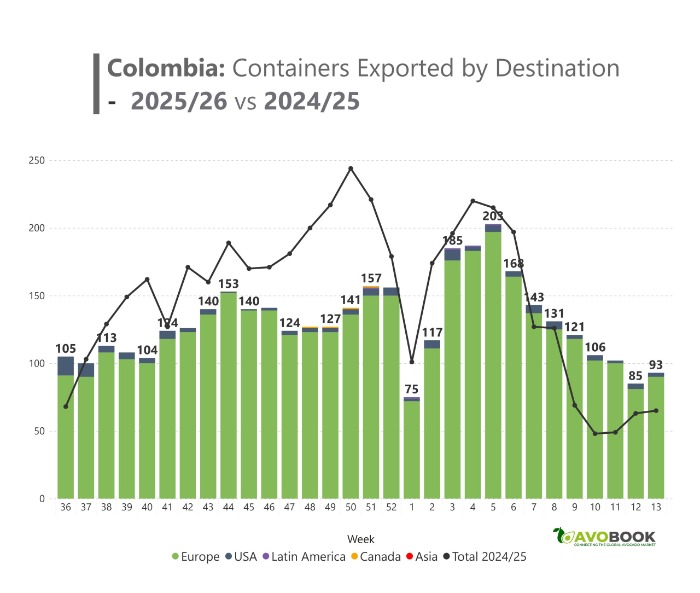

The 2025/26 season shows a more stable curve compared to 2024/25, with a drop in January and a high concentration of shipments to Europe.

The closing of the main Colombian avocado campaign, corresponding to the period September–March 2025/26, shows a more stable behavior compared to the previous season, although maintaining similar patterns at key moments of the cycle.

According to data from Avobook's data team, the current season shows an upward trend during its first few weeks, with no significant week-over-week changes in volume. This trend continues until the first week of 2026, at which point volume drops by almost half. This behavior is not new, as it was also observed in the previous season.

Following this initial drop at the beginning of the year, shipments recovered quickly, reaching weeks with over 200 shipments. After this peak, the curve began to decline gradually, decreasing progressively week by week, until reaching approximately 100 shipments by week 11.

In terms of destinations, the 2025/26 season was marked by a strong concentration in Europe. Approximately 96% of Colombian avocados were destined for this market. The United States accounted for about 3% of shipments, while Canada received less than 1%, with only isolated shipments. Latin America also appears with a practically marginal share of total exports.

When compared to the 2024/25 season, the main difference lies in the shape of the curve. The previous season shows greater volatility, with higher peaks and steeper declines. In fact, that season saw a week with 244 shipments, surpassing the highs observed in the current season.

Similarly, the previous season also shows weeks with considerably lower volumes. From week 10 onwards, shipments hovered around 50 weekly shipments, reflecting a weaker finish compared to the 2025/26 season.

Overall, the analysis reveals that, while structural patterns such as the drop in the first week of the year and the subsequent recovery persist, the current season shows a more stable evolution in its volumes and a less abrupt end, further consolidating a high dependence on the European market as the main destination for Colombian supply.