The Brazilian campaign is picking up pace

Brazil adjusts projections due to increased volumes

Brazil projects a strong increase in shipments from week 12 onwards, with price pressure and Europe absorbing most of the volume.

Brazil is entering a key phase of its avocado campaign, where data is forcing a revision of initial projections in the face of a progressive increase in available volume.

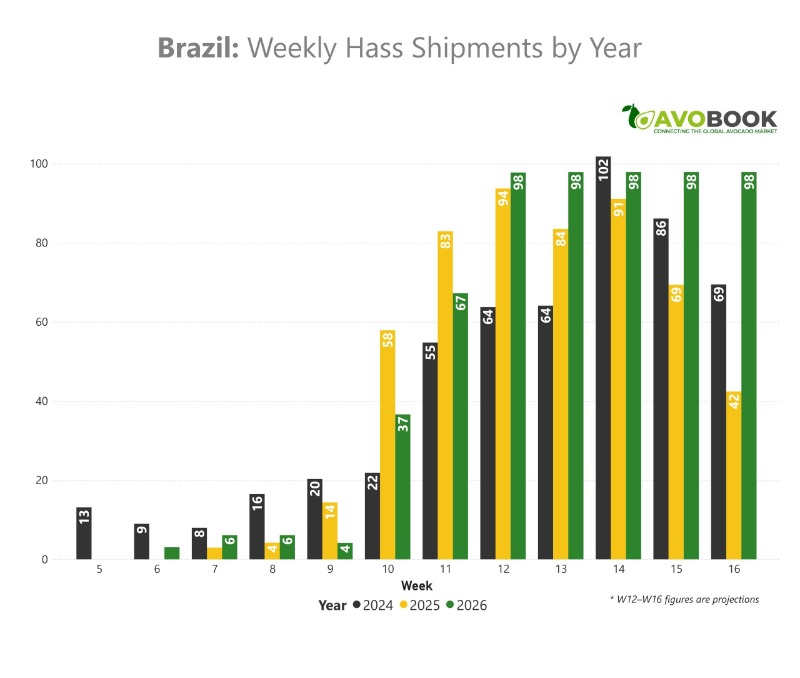

According to Avobook's data team, the behavior of the first weeks of the year shows a clear dynamic: while 2024 had an earlier start, it was 2025 that set the pace with accelerated growth from week 10 onwards. In comparison, 2026 has already surpassed 2024 levels since that same week, although it still remains below the peak observed last year.

However, the focus is not on what has already happened, but on what's to come. Projections indicate that from week 12 onwards, shipments will begin to approach 100 containers per week, a threshold that historically is not usually sustained during this period, but which could be tested this season.

The export program charts reinforce this interpretation. A significant jump is observed between weeks 10 and 13, with a peak in week 11, demonstrating a strong concentration of fruit at the start of the season.

Furthermore, the commercial distribution maintains a marked pattern: Europe concentrates about 75% of shipments up to week 11, consolidating itself as the main destination, while regional markets such as Argentina and Uruguay absorb a smaller but relevant fraction for the price dynamics.

Operational capacity and commercial pressure

On-the-ground analysis confirms that Brazil is entering a stage where the limiting factor is no longer the fruit itself, but the ability to process it and place it on the market.

As Tiago Falanghe Carvalho points out, February saw a lower volume of production due to a lack of fruit at optimal ripeness. This supported prices in the domestic market, particularly at CEAGESP, where they remained firm until early March.

However, this scenario is beginning to change. With packing facilities already operating near maximum capacity—even 24/7 in some cases—the flow of fruit to the market is increasing rapidly. The limitation is no longer one of production but rather one of logistics.

In exports, February marked the gradual start of the season, with Europe leading shipments by a wide margin and FOB prices around USD 1.83/kg. In contrast, regional markets showed an increase in volume, but with a significant drop in prices, especially in Argentina and Uruguay, where prices practically halved between January and February.

This price differential anticipates a scenario of increased market competition. As volume increases from week 12 onward, downward pressure on prices will be inevitable, especially if Europe continues to absorb the majority of the supply.

Meanwhile, some orchards still have below-optimal dry matter levels (21%), which could partially moderate the harvest pace in the short term. However, this does not appear to be a structural constraint, but rather a temporary one given the already expanding supply.

The message is clear: Brazil is entering its most intense campaign phase with a combination of higher volume, high dependence on Europe, and operational capacity stretched to its limit. Market behavior in the coming weeks will be crucial in determining whether this growth can be absorbed without a more significant price adjustment.