US ANALYSIS

Avocado volume falls 10% in the US while prices rise by up to 5%

US volume falls 10% but surpasses 2025. California grows 60%, Mexico declines and prices begin to rebound slightly.

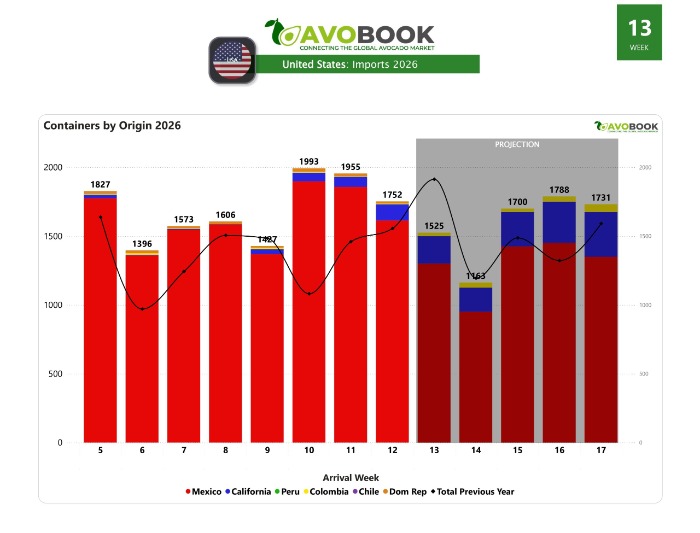

At the close of week 12, the US avocado market showed mixed signals, marked by an adjustment in volumes but with a still solid base year-over-year. Arrivals totaled around 1,750 shipments, representing a 10% drop compared to the previous week, although still 13% above the same period in 2025.

Regarding market composition, Mexico maintains its leading position, although its weekly market share has contracted slightly. California, meanwhile, is beginning to gain ground and has already reached 7% of the market, a typical trend for this time of year. Further behind are the Dominican Republic, with a smaller presence, and the first shipments from Peru, which have yet to achieve a competitive position.

Weekly variations more clearly reflect this realignment. California stands out with a 60% increase in shipments, while Mexico registers a 13% drop and the Dominican Republic declines by 16%, demonstrating an adjustment in supply from some traditional origins.

In terms of prices, week 13 brought a slight increase in most sizes. Sizes 48, 60, and 70 saw increases of between 4% and 5%, while size 84 remained unchanged. Although prices are still below expectations for this time of year, the trend is considered positive, as it consolidates a pattern of gradual increases with no signs of slowing down.

From the outset, adjustments in the market are also noticeable. Antonio Villaseñor points out that farmgate prices are beginning to show a gradual increase, despite the high volumes available. Similarly, Sergio Paz notes that the usual price behavior in Mexico—which tends to rise starting in February or March—has not yet manifested itself with the intensity of other years.

Looking ahead to the coming weeks, the US market is projected to be supplied mainly by Mexico and California, a combination that has historically resulted in greater stability in supply and higher price levels than those observed at the beginning of the year.