Peruvian market

Peru accelerates avocado exports, with Europe leading the way in destinations

The 2026 campaign shows a larger volume and an advance compared to 2025, with Europe consolidating itself as the main destination for Peruvian shipments.

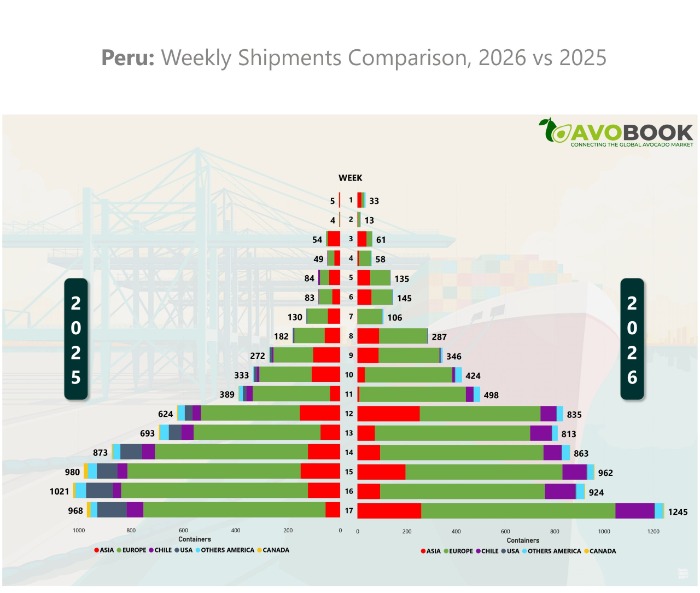

The Peruvian Hass avocado export campaign is progressing more dynamically in 2026, confirming a scenario of earlier production compared to the previous season. This is reflected in comparative data on weekly shipments compiled by the Avobook data team, which shows a faster growth curve and a greater concentration of fruit in key international markets.

Comparing the initial and middle weeks of the season, 2026 shows stronger performance than 2025, especially from week 12 onward, when the difference begins to become apparent. At that point, shipments reached 835 containers compared to 624 recorded during the same period of the previous year, marking the beginning of a gap that gradually widens.

During the following weeks, the trend solidified. In week 13, Peru registered 813 containers compared to 693 in 2015; in week 14, shipments reached 863 compared to 873 the previous year, remaining at high levels; while in week 15, 962 containers were reported, very close to the 980 of the previous season.

However, it is in the most recent weeks where the growth has gained the most momentum. Week 16 closed with 924 containers compared to 1,021 in 2025, but week 17 saw the biggest jump of the season, with 1,245 containers exported, far exceeding the 968 recorded in the same week last year.

This behavior confirms a more intense campaign, with greater fruit availability and an earlier commercial launch, which positions Peru with a stronger supply in the international market.

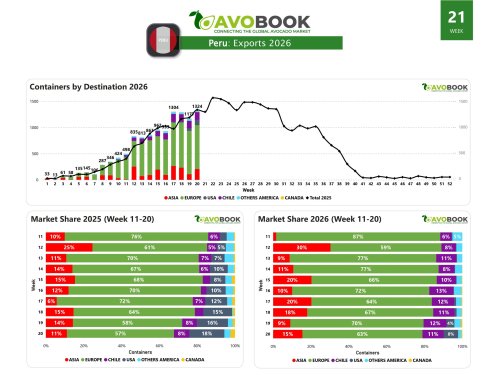

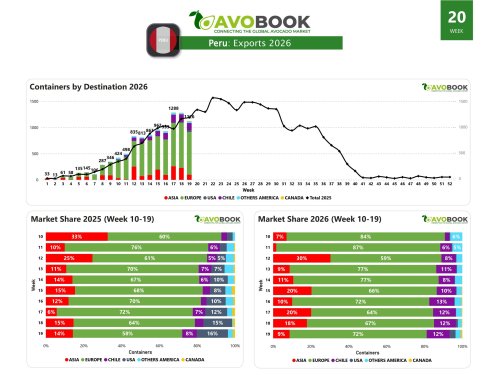

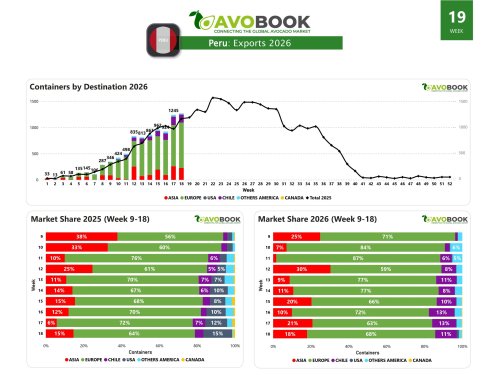

Europe remains, by a wide margin, the main destination for Peruvian exports and accounts for much of this growth. The European market receives the largest share of weekly shipments, solidifying its position as the primary recipient of Peruvian avocados at this stage of the season.

Behind Europe are the United States and Chile, which maintain a more stable share within the export structure. Asia, meanwhile, continues to show a significant presence, although still at a secondary level compared to the weight represented by the European continent.

The strong concentration in Europe is due both to sustained demand and the market's capacity to absorb larger volumes at this stage of the season. This has allowed Peru to maintain a steady flow of fruit and a faster commercial pace compared to 2025.

Overall, the 2026 season is shaping up to be an early campaign, with higher cumulative volume and a clear consolidation of Europe as the main destination. The developments in the coming weeks will be key to determining whether this trend continues and how it will impact the global supply balance during Peru's peak export season.