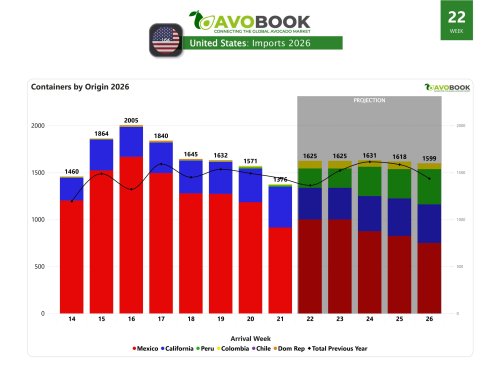

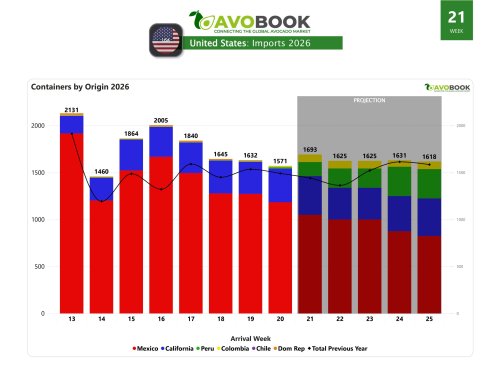

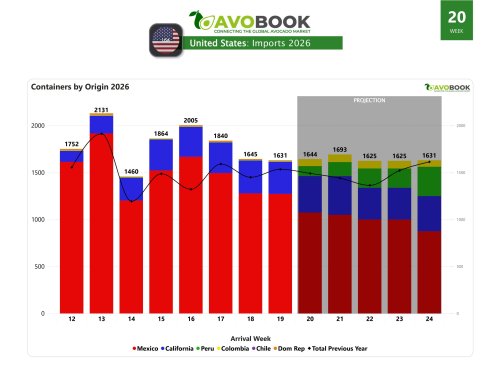

US market

Mexico and California define the avocado supply in the United States

The final stretch in Michoacán would advance with a homogeneous offering, while California enters a phase of greater activity between the end of April and May.

The US avocado market is entering a transitional stage marked by two parallel movements: the final stretch of the Michoacán harvest and California's gradual advance towards more relevant volumes.

According to the views provided by Antonio Villaseñor, director of Aztecavo, and Gary Clevenger, Managing Member and Co-Founder of Freska Produce International, LLC, the end of the Mexican season should not show major surprises, while California has already begun harvesting and is preparing to gain prominence as spring progresses.

In the case of Mexico, Antonio Villaseñor maintains that the harvest in the last quarter will be “very homogeneous.” In his opinion, an increase in volume could be observed around May 5th, although he warns that this movement will coincide with greater activity in California, which would lead to a decrease in Mexican volumes. Therefore, the expected market behavior is not one of sharp fluctuations, but rather a steady outflow throughout the remaining period.

This projection is also linked to market conditions. Villaseñor points out that if a sale were to occur at higher prices, producers would try to take advantage of that opportunity. However, he clarifies that, with the current supply, it seems unlikely that a significant window for better prices will open up. Under this scenario, the prevailing trend would continue to be flat shipments from Mexico, rather than a significant withholding strategy in anticipation of better returns.

Regarding the end of this stage of the campaign, Villaseñor points out that there is always a volume of fruit that carries over to the next season. According to his estimate, there could be around 100,000 tons of old or black fruit in the new campaign. This figure suggests that, even though the overall performance of the final stretch should be orderly, some of the remaining fruit will not necessarily disappear completely within the traditional timeframe, but could overlap with the start of the new cycle.

California enters acceleration phase

On the US side, Gary Clevenger explains that California is already in the early stages of harvesting, but is now entering the period when volumes begin to increase more significantly. He details that as April and May progress, harvesting activity will accelerate, while peak volumes are typically reached from late spring through summer.

Regarding the possibility of waiting for better prices before intensifying the harvest, Clevenger acknowledges that growers may try to temporarily adjust the harvest time at the beginning of the season, especially if the market is oversupplied by Mexico. However, he clarifies that this is not a sustainable strategy in the long run, since fruit maturity, growth pressure, and orchard management are the factors that ultimately determine the decisions. In other words, once the fruit is ready, it should be harvested, regardless of the market situation.

According to Clevenger, the conditions for a massive harvest in California depend on a combination of production and commercial variables. These include crop maturity, with optimal oil levels; warm weather, which accelerates fruit size and ripening; and a high fruit load on the trees. Added to this are market signals: if supply improves or competition decreases, producers gain confidence to harvest more intensively.

For the entire season, current projections for California range between 300 and 330 million pounds. Clevenger describes this volume as a good harvest, though not excessive when compared to total US demand and the volume of weekly Mexican shipments. In other words, California is emerging as a significant player in this phase of the market, but not with a volume capable of single-handedly altering the overall supply balance.

An offer that would not be linear.

Regarding the distribution of Californian fruit, Clevenger anticipates a fluctuating rather than a constant supply. The expected pattern includes a gradual increase in April and May, followed by more robust and consistent production in June and July. Even so, there could be spikes associated with heat waves or promotional demand, as well as occasional slowdowns due to weather or market resistance.

This behavior confirms that California will not enter the harvest with a completely flat curve. On the contrary, its harvest is expected to alternate between periods of higher and lower intensity, typical of its production dynamics. Meanwhile, Mexico is expected to maintain a more homogeneous harvest in the final stretch, although with the possibility of a limited increase toward the beginning of May.

In this context, the US market will operate under a combination of stable Mexican supply and an expanding Californian presence. However, Clevenger emphasizes that prices will continue to be heavily influenced by the industry's total supply, with Mexico setting the pace. This will be further compounded by the potential additional pressure on volume from Peru as its season progresses.

The combined analysis of both sources thus reveals a market facing not an abrupt change in leadership, but rather a gradual transition. Michoacán is expected to continue supplying with relative stability during the final stretch of its harvest, while California will increase its activity between late April and May, with more noticeable growth toward summer. All of this occurs within a context where abundant supply continues to limit the possibility of extended periods of higher prices.